SMM reported on June 30:

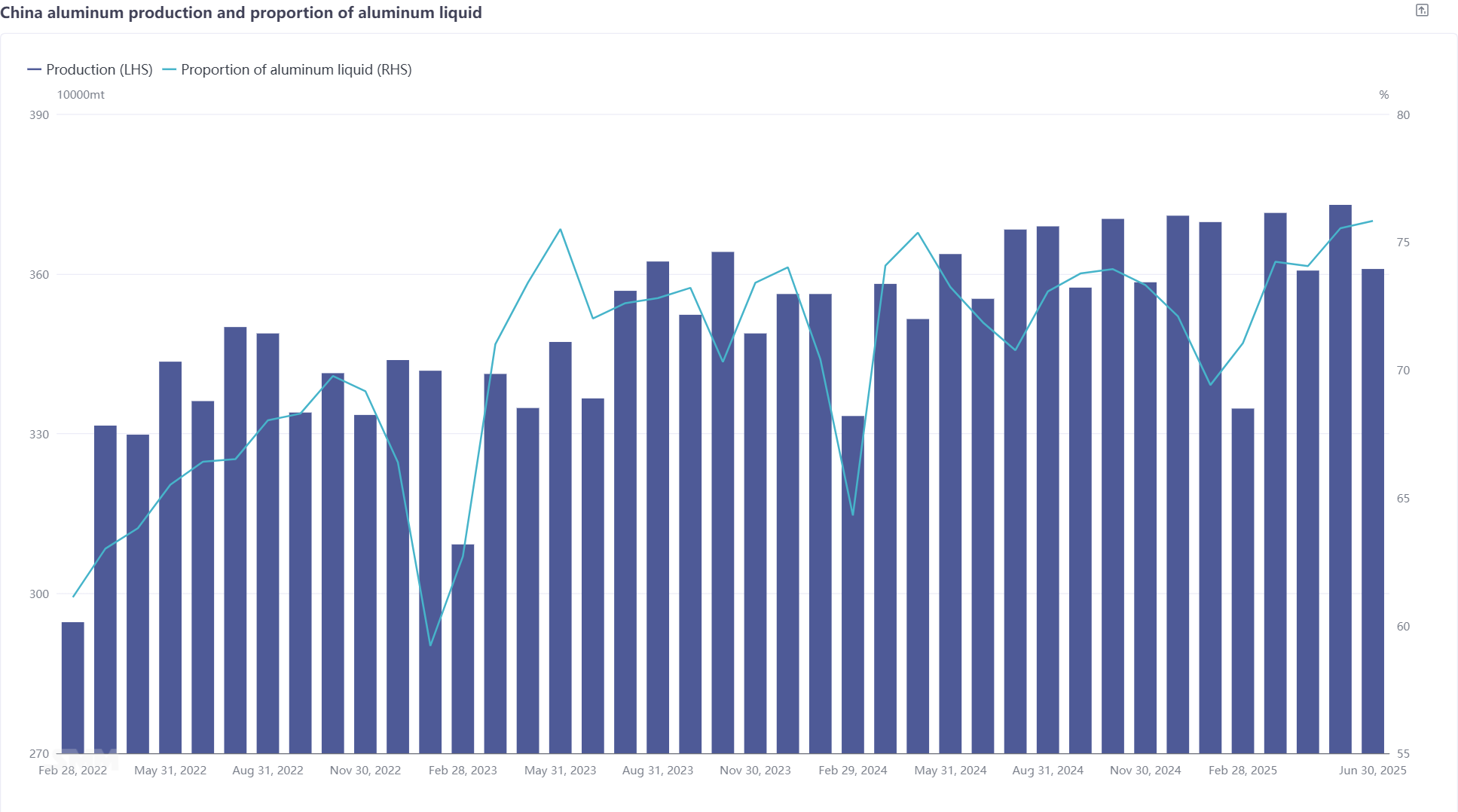

According to SMM statistics, domestic aluminum production in June 2025 (30 days) increased by 1.57% YoY and decreased by 3.23% MoM. The operating capacity of domestic aluminum smelters in June saw a slight MoM fluctuation. SMM learned that the second-phase replacement of aluminum smelters in Shandong-Yunnan began at month-end, requiring production cuts at the original plants and new plant startups only after the replacement capacity passed inspections. The proportion of liquid aluminum in domestic aluminum smelters continued to rise in June, increasing by 0.1 percentage points MoM to 75.8%, with a smaller increase than expected at the beginning of the month, mainly due to high downstream alloy inventory and increased casting ingot production at aluminum plants in some regions. It is expected that the proportion of liquid aluminum will show a downward trend in July. Based on SMM's data on the proportion of liquid aluminum, it is estimated that domestic aluminum casting ingot production in June decreased by 12.77% YoY to approximately 872,500 mt.

Capacity Changes: As of the end of June, SMM estimated that the existing capacity of domestic aluminum smelters was approximately 45.69 million mt (SMM made adjustments in late April, considering capacity replacement and old plant demolitions, and removing some double-counted capacities). The operating capacity of domestic aluminum smelters was approximately 43.83 million mt. Due to capacity replacement, the industry's operating rate decreased slightly MoM. SMM learned that the project of replacing Shandong's capacity with Yunnan's required production cuts at the original plants and new plant startups only after the replacement capacity passed inspections. SMM will continue to monitor changes in aluminum smelter capacity.

Production Forecast: Entering July 2025, the operating capacity of domestic aluminum smelters will remain at highs, with the second batch of replacement projects in Yunnan coming online and the industry's operating rate rebounding. Other projects remain inactive. Regarding the proportion of liquid aluminum, end-use demand has weakened significantly, and there has been a notable inventory buildup of intermediate alloy products. Production cut news has emerged from Qinghai, central China, and other regions, forcing upstream aluminum smelters to increase casting ingot production. The proportion of liquid aluminum may fall to around 74%. Subsequent attention should be paid to the trend of changes in the proportion of liquid aluminum in aluminum smelters, as well as the inventory and demand situation of alloy products.